Private Letter Rulings - IRS Revokes ORGs Exempt Status

GiftLaw Note:

Org is a 501(c)(3) organization founded and operated by President for the purpose of discouraging civil litigation and encouraging ethical behavior in the legal profession. During a recent tax year Org was audited, leading to an investigation as to whether Org should remain tax exempt. Org's activities include producing a quarterly newsletter, maintaining a website and engaging in unrelated business income (UBI) activities. President is Org's only employee. Org has no other volunteers, employees or members. Org's articles of incorporation state that President will receive payment for his services of 15% of the annual gross profits of Org. However, Org did not issue any Form 1099 or W-2 for the audit year. In addition, the agent found questionable transactions that did not further Org's exempt purpose. When asked, President said these transactions were for the repayment of a loan he made to Org. No records were provided substantiating the loan transaction. In addition, Org received payment for agreeing to file a writ of mandamus and preparing contact letters to sue lawyers, judges and the State. The contract identified this payment for services as tax deductible.

Under Sec. 1.501(c)(3)-1 an organization will not be considered operated exclusively for exempt purposes if any part of its net earnings inure to the benefit of a private individual or if more than an insubstantial part of its activities is not in furtherance of an exempt purpose. In Indiana Retail Hardware Association v. United States, 366 F.2d 998 (Ct. Cls. 1966), the court ruled that if UBI comprised a substantial portion of an exempt organization's income, loss of tax-exempt status might result. First, Org had UBI during the year of the audit equal to 71% of its total receipts. Second, the service was unable to find evidence that Org primarily engaged in exempt activities. The documents provided detailed the personal activities of President and payments that inured to the benefit of President. Finally, Sec. 501(c)(3) states that organizations may not participate or intervene in any political campaign on behalf of any candidate for public office. When President entered the race for governor of State, President used Org's funds for her campaign. As a result, the Service revoked Org's exempt status.

Under Sec. 1.501(c)(3)-1 an organization will not be considered operated exclusively for exempt purposes if any part of its net earnings inure to the benefit of a private individual or if more than an insubstantial part of its activities is not in furtherance of an exempt purpose. In Indiana Retail Hardware Association v. United States, 366 F.2d 998 (Ct. Cls. 1966), the court ruled that if UBI comprised a substantial portion of an exempt organization's income, loss of tax-exempt status might result. First, Org had UBI during the year of the audit equal to 71% of its total receipts. Second, the service was unable to find evidence that Org primarily engaged in exempt activities. The documents provided detailed the personal activities of President and payments that inured to the benefit of President. Finally, Sec. 501(c)(3) states that organizations may not participate or intervene in any political campaign on behalf of any candidate for public office. When President entered the race for governor of State, President used Org's funds for her campaign. As a result, the Service revoked Org's exempt status.

Dear * * *:

In a determination letter dated November 19, 20XX, you were held to be exempt from Federal income tax under section 501(c)(3) of the Internal Revenue Code (the Code).

Based on recent information received, we have determined you have not operated in accordance with the provisions of section 501(c)(3) of the Code. Accordingly, your exemption from Federal income tax is revoked effective January 1, 20XX. This is a final adverse determination letter with regard to your status under section 501(c)(3) of the Code.

We previously provided you a report of examination explaining why we believe revocation of your exempt status is necessary. At that time, we informed you of your right to contact the Taxpayer Advocate, as well as your appeal rights.

Our adverse determination was made for the following reasons:

You have failed to demonstrate that you are operated exclusively for exempt purposes, and that no part of your net earnings inures to the benefit of private shareholders and individuals, as required by section 501(c)(3) of the Code. In addition, your activities more than insubstantially further non-exempt purposes, and you operate primarily for the benefit of private rather than public interests.

Contributions to your organization are no longer deductible under section 170 of the Internal Revenue Code. You are required to file Federal income tax returns on Form 1120. Those returns should be filed with the appropriate Service Center.

Processing of income tax returns and assessment of any taxes due will not be delayed should a petition for declaratory judgment be filed under section 7428 of the Internal Revenue Code.

If you decide to contest this determination in court, you must initiate a suit of declaratory judgment in the United States Tax Court, the United States Claims Court or the District Court of the United States for the District of Columbia before the 91st day after the date this determination was mailed to you. Contact the clerk of the appropriate court for rules for initiating suits for declaratory judgment. You may write to the Tax Court at the following address:

United States Tax Court,

400 Second Street NW

Washington, D.C. 20217

You also have the right to contact the office of the Taxpayer Advocate. You can call 1-877-777-4778 and ask for Taxpayer Advocate assistance. If you prefer, you may contact your local Taxpayer Advocate at:

Internal Revenue Service

Office of the Taxpayer Advocate

* * *

Taxpayer Advocate assistance cannot be used as a substitute for established IRS procedures, formal appeals processes, etc. The Taxpayer Advocate is not able to reverse legal or technically correct tax determinations or extend the time fixed by law that you have to file a petition in the United States Tax Court. The Taxpayer Advocate, can, however, see that a tax matter, that may not have been resolved through normal channels, gets prompt and proper handling.

We will notify the appropriate State Officials of this action, as required by section 6104(c) of the Internal Revenue Code.

If you have any questions in regards to this matter please contact the person whose name and telephone number are shown in the heading of this letter.

Thank you for your cooperation.

Sincerely yours,

Margaret Von Lienen

Director, EO Examinations

03/10/2014

Dear * * *:

WHY YOU ARE RECEIVING THIS LETTER

We propose to revoke your status as an organization described in section 501(c)(3) of the Internal Revenue Code. Enclosed is our report of examination explaining the proposed action.

WHAT YOU NEED TO DO IF YOU AGREE

If you agree with our proposal, please sign the enclosed Form 6018, Consent to Proposed Action -- Section 7428, and return it to the contact person at the address listed above (unless you have already provided us a signed Form 6018). We'll issue a final revocation letter determining that you aren't an organization described in section 501(c)(3).

After we issue the final revocation letter, we'll announce that your organization is no longer eligible for contributions deductible under section 170 of the Code.

IF WE DON'T HEAR FROM YOU

If you don't respond to this proposal within 30 calendar days from the date of this letter, we'll issue a final revocation letter. Failing to respond to this proposal will adversely impact your legal standing to seek a declaratory judgment because you failed to exhaust your administrative remedies.

EFFECT OF REVOCATION STATUS

If you receive a final revocation letter, you'll be required to file federal income tax returns for the tax year(s) shown above as well as for subsequent tax years.

WHAT YOU NEED TO DO IF YOU DISAGREE WITH THE PROPOSED REVOCATION

If you disagree with our proposed revocation, you may request a meeting or telephone conference with the supervisor of the IRS contact identified in the heading of this letter. You also may file a protest with the IRS Appeals office by submitting a written request to the contact person at the address listed above within 30 calendar days from the date of this letter. The Appeals office is independent of the Exempt Organizations division and resolves most disputes informally.

For your protest to be valid, it must contain certain specific information including a statement of the facts, the applicable law, and arguments in support of your position. For specific information needed for a valid protest, please refer to page one of the enclosed Publication 892, How to Appeal an IRS Decision on Tax-Exempt Status, and page six of the enclosed Publication 3498, The Examination Process. Publication 3498 also includes information on your rights as a taxpayer and the IRS collection process. Please note that Fast Track Mediation referred to in Publication 3498 generally doesn't apply after we issue this letter.

You also may request that we refer this matter for technical advice as explained in Publication 892. Please contact the individual identified on the first page of this letter if you are considering requesting technical advice. If we issue a determination letter to you based on a technical advice memorandum issued by the Exempt Organizations Rulings and Agreements office, no further IRS administrative appeal will be available to you.

CONTACTING THE TAXPAYER ADVOCATE OFFICE IS A TAXPAYER RIGHT

You have the right to contact the office of the Taxpayer Advocate. Their assistance isn't a substitute for established IRS procedures, such as the formal appeals process. The Taxpayer Advocate can't reverse a legally correct tax determination or extend the time you have (fixed by law) to file a petition in a United States court. They can, however, see that a tax matter that hasn't been resolved through normal channels gets prompt and proper handling. You may call toll-free 1-877-777-4778 and ask for Taxpayer Advocate assistance. If you prefer, you may contact your local Taxpayer Advocate at:

Internal Revenue Service

Office of the Taxpayer Advocate

* * *

FOR ADDITIONAL INFORMATION

If you have any questions, please call the contact person at the telephone number shown in the heading of this letter. If you write, please provide a telephone number and the most convenient time to call if we need to contact you.

Thank you for your cooperation.

Sincerely,

Nanette M. Downing

Director, EO Examinations

ISSUE(S)

Whether * * * continues to qualify for exemption under Section 501(c)(3) of the Internal Revenue Code.

FACTS

The organization was granted exemption under 501(c)(3) of the Internal Revenue Code per a determination letter issued November 19, 20XX. The organization was founded and operated by * * *, who serves as its President. Based on the determination application and its Articles of Incorporation, the organization purposes are:

a) To discourage civil litigation

b) To increase public awareness of the illegal and unethical practices of many attorneys

c) To reduce stress and save people money

d) To keep attorneys honest

e) To gain respect for the legal profession

t) To improve the legal system in America

g) To seek "justice for all"

h) To cooperate with all public, private, religious agencies and professional groups in the furtherance of these ends

i) To financially support and promote the common cause

j) To solicit and receive fund for the accomplishment of the above purposes

During the years under audit, the organization's activities consisted of producing a quarterly newsletter, maintaining the organization's website, and UBI related activities. * * * conducted these activities. The organization had no other members, volunteers, or employees. The agent reviewed the organization's business records, including minutes, bank statements, and newsletter. * * * did not provide any newsletter. The agent was able to download a copy of the newsletter from the organization website. * * * only provides bank statements. No other financial information was provided.

On April 29, 20XX the agent held an initial interview with * * *. During the interview, * * * said the organization did not have any employees and that none of the officers or directors are compensated. The organization did not issue any Form 1099 for contract labor or W-2 for wages for the years under audit.

Under the organization's Articles of Incorporation, Article II, Section 2 states "No part of any net earning shall inure to the benefit of any member or individual, and only the Chief Executive Officer (CEO)/Board President of the Association shall receive a salary for his/her services." Under the organization Bylaws, Article VII states, "the CEO shall receive a salary in the amount of 15% of the annual gross profits of the * * *" (Exhibit E.1-7)

For the years under audit, the organization listed * * *, * * * and * * * as the organization's board of directors. * * * managed the organization day-to-day operation. * * * is the only person in the organization.

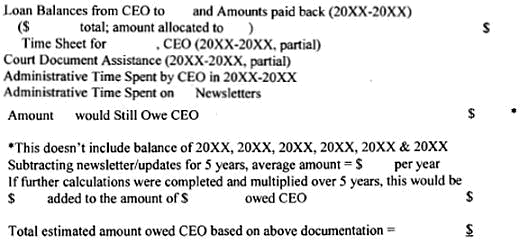

The agent reviewed the organization's bank statements and identified questionable transactions that did not seems to further the organization's exempt purpose. These transactions were with various vendors, including * * *, * * *, * * *, * * *, and * * * (Exhibit A.1). The agent presented these questionable transactions to * * * for explanation and requested receipts or documentation to support exempt purposes. * * * did not provide any supporting documentation to substantiate the nature of these transactions. Subsequent to this request, said these transactions were for the repayment of a loan * * * made to the organization. The agent requested documentation to support the loan balance. * * * reconstructed the loan transactions and presented the agent with a list of items. (Exhibit C.1) No records were produced to substantiate any of the items reflected in the listing.

On August 15, 20XX, the organization entered into a contract with * * *. Per the contract, organization would file a writ of mandamus and prepare contact letters to sue lawyers, judges, and the State of * * *. The organization was paid $* * * for this service. Per the contract, the payment of $* * * is identified as a donation and tax deductible. The contract also states, "additional donation may be requested and must be produced in a timely manner." (Exhibit B.2-1)

During the review of the bank statements, the agent found a check written to "cash". The memo section the check reflected "cash for campaign". The agent asked * * * to provide the exempt purpose of this payment. * * * said this check was for repayment of the loan.

LAW

§ 1.501(c)(3)-1 Organizations organized and operated for religious, charitable, scientific, testing for public safety, literary, or educational purposes, or for the prevention of cruelty to children or animals. In order to be exempt as an organization described in section 501(c)(3), an organization must be both organized and operated exclusively for one or more of the purposes specified in such section. If an organization fails to meet either the organizational test or the operational test, it is not exempt.

Operational Test:

1) Primary activities. An organization will be regarded as operated exclusively for one or more exempt purposes only if it engages primarily in activities which accomplish one or more of such exempt purposes specified in section 501(c)(3). An organization will not be so regarded if more than an insubstantial part of its activities is not in furtherance of an exempt purpose.

2) Distribution of earnings. An organization is not operated exclusively for one or more exempt purposes if its net earnings inure in whole or in part to the benefit of private shareholders or individuals.

26 USC § 513 -- UNRELATED TRADE OR BUSINESS The term "unrelated trade or business" means, in the case of any organization subject to the tax imposed by section 511, any trade or business the conduct of which is not substantially related (aside from the need of such organization for income or funds or the use it makes of the profits derived) to the exercise or performance by such organization of its charitable, educational, or other purpose or function constituting the basis for its exemption under section 501(c)(3)),

Treasury Regulations section 1.501(c)(3)-1(d)(1)(ii) states that the burden of proof is upon the organization to establish that it is not organized or operated for the benefit of private interests. This requirement applies equally to inurement and private benefit issues. While it is difficult to prove a negative, the organization is certainly in a better position than the Service to know the detailed facts surrounding its formation and operation. Therefore, in an exemption application case the organization is required to furnish the Service with the documents setting forth its purposes and rules of operation as well as a detailed explanation of its operations. See Rev. Proc. 84-46, 1984-1 C.B. 541.

Treasury Regulations section 1.62-2(c)(2)(c) Reimbursement or other expense allowance arrangement -- (1) Defined. For purposes of §§ 1.62-1, 1.62-1T, and 1.62-2, the phrase "reimbursement or other expense allowance arrangement" means an arrangement that meets the requirements of paragraphs (d) (business connection, (e) (substantiation), and (f) (returning amounts in excess of expenses) of this section. A payor may have more than one arrangement with respect to a particular employee, depending on the facts and circumstances. See paragraph (d)(2) of this section (payor treated as having two arrangements under certain circumstances). (2) Accountable plans -- (i) In general. Except as provided in paragraph (c)(2)(ii) of this section, if an arrangement meets the requirements of paragraphs (d), (e), and (f) of this section, all amounts paid under the arrangement are treated as paid under an "accountable plan."

Treasury Regulations section 1.274-5T(2)(c)(i) In general. -- To meet the "adequate records" requirements of section 274(d), a taxpayer shall maintain an account book, diary, log, statement of expense, trip sheets, or similar record, and documentary evidence which, in combination, are sufficient to establish each element of an expenditure or use specified in paragraph (b) of this section. It is not necessary to record information in an account book, diary, log, statement of expense, trip sheet, or similar record which duplicates information reflected on a receipt so long as the account book, etc., and receipt complement each other in an orderly manner.

Founding Church of Scientology v. United States, 412 F.2d 1197 (Ct. Cl. 1969), cert. den., 397 U.S. 1009 (1970), an organization argued that it had paid its founder for expenses incurred in connection with his services, made reimbursements to him for expenditures on its behalf, and made some payments to him as repayments on a loan. The organization could produce no evidence of contractual agreements for services, documents evidencing indebtedness, or any explanation regarding the purposes for which expenses had been incurred.

Indiana Retail Hardware Association v. U.S., 366 F.2d 998 (Ct. Cls. 1966) If unrelated business income comprises a "substantial" portion of an exempt organization's income, loss of tax-exempt status may result.

Arlie Foundation v. IRS 283 F Supp 2d 58 (D.D.C 2003) the district court found that the operational test requires both an organization engage "primarily" in activities that accomplish its exempt purpose and that not more than an "insubstantial part of its activities" further a non-exempt purpose. Though an incidental non-exempt purpose will not automatically disqualify an organization, the "presence of a single nonexempt purpose, if substantial in nature, will destroy the exemption, regardless of the number of importance of truly exempt purposes."

Rev. Rul. 71-447, 1971-2 C. B. 230 Violation of constitutionally valid laws is inconsistent with exemption under IRC 501(c)(3). As a matter of trust law, one of the main sources of the general law of charity, planned activities that violate laws are not in furtherance of a charitable purpose. "A trust cannot be created for a purpose which is illegal. The purpose is illegal . . . if the trust tends to induce the commission of crime or if the accomplishment of the purpose is otherwise against public policy . . . Where a policy is articulated in a statute making certain conduct a criminal offense, then . . ., a trust is illegal if its performance involves such criminal conduct, or if it tends to encourage such conduct." Thus, all charitable trusts (and by implication all charitable organizations, regardless of their form) are subject to the requirement that their purpose may not be illegal or contrary to public policy.

GOVERNMENT POSITION

In accordance with the above-cited provisions of the Code and Regulations under 501(c)(3), Treasury Regulation § 1.501(c)(3), and court cases listed above, the * * * is not the type of an organization for which an exemption from tax was intended. The following is a list of issues; anyone of them would disqualify from tax exemption:

1. Operational Test -- § 1.501(c)(3)-1 For an organization to be exempt as an organization described in section 501(c)(3) it has to meet the operational test. An organization will not be so regarded if more than an insubstantial part of its activities is not in furtherance of an exempt purpose. The contract between * * * and the * * * is contract for payment for services. The services provided are not part of the organization exempt purpose. The income received this service is considered unrelated business income and is taxable under Form 990-T. The organization did not file a Form 990-T. For the audit year 20XX the organization had $* * * of UBI on total deposits of $* * * (71%) of total income which is considered "substantial. Based on Indiana Retail Hardware Association v U.S., 366 F.2d 998 (Ct. Cls. 1966) if unrelated business income comprises a "substantial" portion of an exempt organization income, loss of tax-exempt status may result.

2. Lack of Exempt Activities -- The agent analyzed the organization minutes (Exhibit E.2), newsletter (Exhibit E.3), and bank statements for the organization activities. The majority of the minutes discuss personal activities of * * *. The agent was unable to find any evidence of the organization primarily activities were for exempt purposes in the minutes. The agent reviewed the organization newsletter. The newsletter contains news updates and information regarding * * *. * * * is father. * * * had * * * body exhumed and DNA tested with organization funds. The agent was unable to find any evidence of the organization primarily activities were for exempt purposes. The agent analyzed the organization bank statements. Most of the expenditures were for * * * personal benefit. The agent was unable to find any expenditures to support the organization primarily activities were for exempt purposes.

3. Distribution of earnings -- An organization is not operated exclusively for one or more exempt purposes if its net earnings inure in whole or in part to the benefit of private shareholders or individuals. Regs. 1.501(c)(3)-1(d)(1)(ii) states that the burden of proof is upon the organization to establish that it is not organized or operated for the benefit of private interests. This requirement applies equally to inurement and private benefit issues. In this case, the Agent identified questionable transactions from the business bank account that were not substantiated for an exempt purpose. These transactions appear to be personal and for the benefit of * * *. These payments are $* * * for 20XX, $* * * for 20XX, and $* * * for 20XX. These payments were not reported as wages or reimbursements. See Exhibit A.1 for detail of these payments.

4. Political Campaign -- 100 Cong. Rec. 9,604 (1954) IRC 501(c)(3) organizations may not "participate in, or intervene in (including the publishing or distributing of statements), any political campaign on behalf of any candidate for public office." Around that time, * * * entered the race for governor of * * *. * * * used * * * funds for her campaign for governor (Exhibit A.2-10 Check #1519 and Exhibit C.1).

TAXPAYER POSITION

* * * claimed that all the questionable transactions identified from the organization's checking account were repayments of monies owed to her by the organization. The agent requested information to substantiate the loan balance. * * * had no documentation and did not know the amount of the loan balance. Subsequently, reconstructed loan transactions for a loan balance of $* * *. (Exhibit C.1)

CONCLUSION

The organization has several violations that jeopardize its exempt status: 1) the organization has no exempt activities and no records to support exempt activities, 2) the organization has substantial income from unrelated business income, 3) inurement to * * *, and 4) the organization made a prohibited political contribution. All of these issues are in violation of 501(c)(3).

The agent reviewed information supplied by * * * to support her claim of an outstanding loan from her to the organization. (Exhibit C.1). The document included the following listing:

1) According to * * *, the organization owes her $* * * authoring a book. The organization would also cover all cost of publishing, promoting, marketing, and selling the book. * * * would receive payment of 15% of all gross profits. The agent reviewed the contract between * * * and * * * regarding the book (Exhibit D.1). The contract was sign by * * * for both parties. There were no board member signatures. The contract has no basis or analysis on the payment of $* * * if it is an arm's length transaction and in the best interest of the organization. The agent determines this transaction is per se Private Inurement and the agent cannot consider the private benefit received from the organization to as repayment of this debt.

2) The agent was unable to verify if the list of expenses was either for the organization or * * * benefit. For example, there were payment made to credit cards without identifying item or services paid for; business lunch with no receipts, name of the persons attending, and purpose; utilities payments (the organization does not own any real properties), DirectTV, medical payments, gas and car maintenance (the organization does not owns any automobiles), etc. The agent request backup documents supporting these claims from * * * but * * * refused to provide any additional documents. * * * did not provide any of * * * bank statements between 20XX to 20XX and the agent was unable to verify any draws * * * may have made from the organization bank account between those periods. Since the agent was unable to verify the loan balance owe to * * * from the organization due to the lack of supporting documents, the agent cannot contribute private benefits * * * identified in Exhibit A.1 as repayment of an outstanding loan since the agent cannot verify an existence of the loan.

3) * * * claims that the organization owes her $* * * for time-spent working for the organization. Yet, there is no record of wages payable and there is no issuance of W-2 or 1099. Also the organization bylaws states "the CEO shall receive a salary in the amount of 15% of the annual gross profits of the * * * (Exhibit E.1-7)." The organization average less than $* * * per year (Exhibit C.1-15) so base on that figure the total salary * * * could receive between year 20XX to 20XX is $* * *. Since there were no documentation regarding the organization wages balance owe to * * * and the non-filing of W-2 and 1099, the private benefit * * * receives identified by the agent (Exhibit A.1) cannot be classified as payment of wages.

The Government concludes that the Exempt Organizations, * * *, does not meet the requirements to be recognized as exempt from federal income tax under 501(c)(3) of the Internal Revenue Code. Accordingly, the organization's exempt status should be revoked effective January 1, 20XX.